Canadian Occupational Projection System (COPS)

Industrial Summary

Oil and Gas Extraction

(NAICS 2111)

This industry comprises establishments primarily engaged in operating oil and gas field properties, such as exploration for crude petroleum and natural gas, drilling, completing and equipping wells, and other related activities in the preparation of oil and gas. It includes both the production from wells using traditional pumping techniques and the production from surface shale or tar sands using non-conventional techniques. Non-conventional production is accounting for more than 50% of total domestic production. Canada is the fourth-largest producer of crude oil and the sixth-largest producer of natural gas in the world. Alberta has always been the dominant producer in the country, supplying about three-quarters of total production of oil and gas, followed by British Columbia (mostly gas), Saskatchewan (mostly oil), and Newfoundland-Labrador (oil). About 80% of crude oil and about 45% of natural gas produced in Canada are exported, mainly to the United States. On the other hand, about 40% of the crude oil used in domestic refineries and about 20% of the natural gas consumed in the country are imported[1]. The industry employed about 97,900 workers in 2023, mostly concentrated in Alberta (82%), with a workforce primarily composed of men (78%). Wages are among the highest across the country, with the average wage being almost twice as high as the all-industry average.

Key occupations (5-digit NOC) include:

- Oil and gas drillers, servicers, testers and related workers (83101)

- Contractors and supervisors, oil and gas drilling and services (82021)

- Petroleum engineers (21332)

- Central control and process operators, petroleum, gas and chemical processing (93101)

- Managers in natural resources production and fishing (80010)

- Purchasing agents and officers (12102)

- Power engineers and power systems operators (92100)

- Geoscientists and oceanographers (21102)

- Heavy-duty equipment mechanics (72401)

- Construction millwrights and industrial mechanics (72400)

- Industrial instrument technicians and mechanics (22312)

- Steamfitters, pipefitters and sprinkler system installers (72301)

- Oil and gas drilling, servicing and related labourers (85111)

- Oil and gas well drilling and related workers and services operators (84101)

- Geological and mineral technologists and technicians (22101)

Projections over the 2024-2033 period

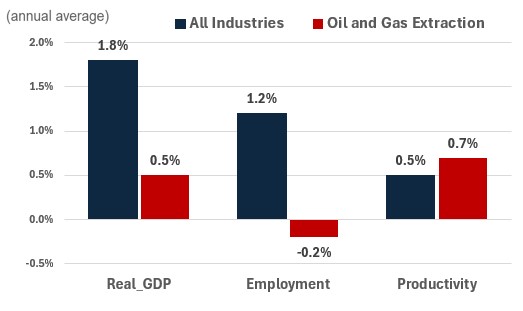

Real GDP is projected to grow at an average annual rate of 0.5%. In the short-term, the opening of the Transmountain Pipeline Expansion is expected to provide a significant boost to the industry output growth. It is projected to support continued flow of oil to the United States, but also allow greater access to international markets. In addition, the inauguration of LNG Canada operations, expected in 2025, will add to the country natural gas export capacity. However, the introduction of the federal government’s 2030 Emissions Reduction Plan, which targets a reduction in greenhouse gas emissions of 40% below 2005 levels by 2030, is expected to negatively impact the industry in the second half of the projection period.

Productivity is expected to grow at an average annual rate of 0.7%. Gains in productivity reflect projected advancements in extractive technology and modular facility design. While productivity growth is expected, it should be modest relative to what has been observed prior to the pandemic. Uncertainty regarding the impact of the green transition is expected make businesses more cautious with their capital spending intentions. In addition, the shift in the lifecycle of oil sand production (which is highly capital intensive) from its growth phase to its mature phase will lead to more modest productivity gains.

Employment is projected to decline by 0.2% annually. Employment growth is expected to follow a similar path than output, with gains in the short-term, but losses in the second half that are expected to offset the early growth. It is projected that productivity growth will account for most of the output growth, as it did in the previous decade. Overall, employment prospect will be very limited, especially over the longer term.

Challenges and Opportunities

In the projection, it is assumed that the sector will be able to partially achieve the cap constrain on greenhouse gas emissions from continued improvement in production efficiency (emissions per unit of output) and emission reductions from actions related to abatement of methane associated with fugitive and venting related sources. Reaching the cap will also require significant investments in carbon capture and storage (CCS) and/or a reduction in production activity and resulting emissions.

Curtailing production is expected to yield higher asset value than investments in CCS (carbon capture and storage) technology in order to meet mandatory emission caps. In other words, from a purely financial perspective, reducing output might be a more attractive option than rapidly investing in CCS.

Overall, the projection assumes that investment in CCS technology alone will not be enough to reach the 2030 target and production cuts in some industries, most notably oil and gas extraction, will be necessary.

Real GDP, Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Oil and Gas Extraction | 0.5 | -0.2 | 0.7 |