Canadian Occupational Projection System (COPS)

Industrial Summary

Food and Beverage Products

(NAICS 3111-3119; 3121; 3122; 3123)

This industry comprises establishments primarily engaged in manufacturing food as well as beverage and tobacco products. Food manufacturing is by far the most important segment, accounting for 80% of production in 2023, followed by beverage products (16%) and tobacco products (4%). The industry is largely domestic-oriented as about two thirds of its production is sold within the country. However, foreign markets are representing an increasing share of total sales, with exports accounting for 34% of revenues, up from 24% a decade ago. With about 328,500 workers in 2023, it is the largest employer in the manufacturing sector (18% of all manufacturing workers). Most workers are employed in food manufacturing (84%) and employment in the industry is largely concentrated in Ontario (36%) and Quebec (26%), with men accounting for 59% of the workforce. Key occupations (5-digit NOC) include:[1]

Key occupations (5-digit NOC) include:

- Process control and machine operators, food and beverage processing (94140)

- Labourers in food and beverage processing (95106)

- Supervisors, food and beverage processing (92012)

- Industrial butchers and meat cutters, poultry preparers and related workers (94141)

- Testers and graders, food and beverage processing (94143)

- Bakers (63202)

- Labourers in fish and seafood processing (95107)

- Fish and seafood plant workers (94142)

Projections over the 2024-2033 period

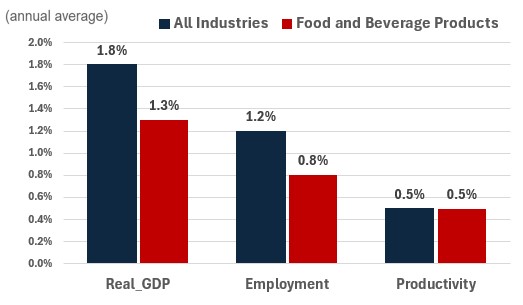

Real GDP is projected to grow at an average annual rate of 1.3%. Output growth in the food and beverage manufacturing industry is projected to be supported by robust population growth. The trend for healthier food, including the choice of some consumers to have higher quality, locally sourced and ethically produced goods in a more transparent ecosystem will also benefit Canadian producers. The export-oriented segment of the industry is expected to continue to be supported by a relatively low Canadian dollar and further expansion into new international markets. While tobacco consumption is projected to keep declining, further growth in the manufacturing of cannabis products is expected to partially offset this loss.

Productivity is expected to grow at an average annual rate of 0.5%. The sector has seen reduced profit margins in recent years as consumers, faced with higher food prices, began purchasing more items on sale, substituting to less expensive brands, shopping more often at low-cost retailers and reducing on the amount of food purchased[2]. To increase margins, manufactures are likely to prioritize productivity-enhancing investments such as the increased use of robotics in production facilities. The industry should be receptive to technologies that reduce wastage through better detection of food contamination, along with biotechnologies that can help insulating food, beverage and tobacco production from seasonal and weather-related fluctuations common in the agriculture industry.

Employment is projected to increase by 0.8% annually. Faced with a relative solid outlook for output growth, employment is expected to grow at a healthy pace, but job creation should continue to be restrained by additional productivity gains.

Challenges and Opportunities

Higher food prices led to some changes in consumer shopping habits over the past years. If these behaviour shifts continue, producers might continue to experience reduced profit margins. However, with most of the population growth stemming from international immigration, the country’s food preferences are becoming more diverse, offering opportunities for food manufacturers to serve niche – but growing – market segments. Even though the industry is not as dependent on exports as other manufacturing industries, the United States’ threat to impose new tariffs on imports from Canada (which was not incorporated into the projections) constitutes a major source of uncertainty and, if it materializes, would represent a significant burden on the industry.

Real GDP , Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Food and Beverage Products | 1.3 | 0.8 | 0.5 |

[1]Key occupations for manufacturing industries in general also include: Manufacturing managers (90010); Construction millwrights and industrial mechanics (72400); Material handlers (75101); Shippers and receivers (14400); Transport truck drivers (73300); Industrial engineering and manufacturing technologists and technicians (22302); Industrial electricians (72201); and Industrial and manufacturing engineers (21321).

[2]Farm Credit Canada, FCC Food and Beverage Report, 2024.