Canadian Occupational Projection System (COPS)

Industrial Summary

Paper Manufacturing

(NAICS 3221; 3222)

This industry comprises establishments primarily engaged in manufacturing pulp and paper as well as converted paper products (such as paperboard boxes, corrugated boxes, fibre boxes and sanitary food containers). Pulp and paper is the most important of the two segments, accounting for 59% of production in 2023. Overall, the industry is export intensive with about 58% of its revenues coming from foreign markets, of which about two-thirds are from the United States. The two segments, however, do not face the same degree of exposure to domestic and foreign economic conditions. Converted paper is highly dependent on domestic demand, with 69% of its production sold within the country. In contrast, pulp and paper is far more sensitive to foreign demand, with exports accounting for about 80% of its production, largely shipped to the United States (59% of exports) and China (22%). The industry employed about 57,500 workers in 2023 (3.2% of total manufacturing employment), with 64% in pulp and paper and 36% in converted paper products. Employment is mainly concentrated in Quebec (35%), Ontario (29%) and British Columbia (17%), and the workforce is primarily composed of men (80%).

Key occupations (5-digit NOC) include:

- Pulp mill, papermaking and finishing machine operators (94121)

- Labourers in wood, pulp and paper processing (95103)

- Paper converting machine operators (94122)

- Supervisors, forest products processing (92014)

- Power engineers and power systems operators (92100)

- Chemical engineers (21320)

- Pulping, papermaking and coating control operators (93102)

Projections over the 2024-2033 period

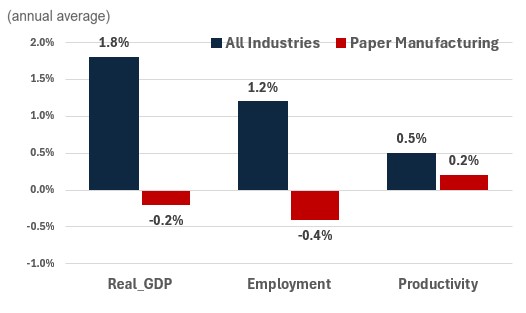

Real GDP is projected to decline at an average annual rate of 0.2%. The predominance of electronic media will continue to reduce the demand for traditional paper and newsprint, but it is expected that the declining trend in output will slowdown relative to the past decade. E-commerce sales is one factor that is supporting growth in the industry through demand for packaging materials. The outlook for sanitary paper products also remains positive, supported by rising demand in both emerging and mature markets. Efforts to reduce the prevalence of single-use plastics present opportunities for the paper manufacturing industry to grow by offering sustainable alternatives (for example, paper instead of plastic bags).

Productivity is expected to grow at an average annual rate of 0.2%. Modest gains are expected as producers facing lower sales volumes may be reluctant to invest massively in machinery and equipment. However, growing production from competing suppliers in South America and Asia will keep putting pressures on Canadian manufacturers to consolidate operations, as firms in these regions are able to produce at lower costs and can also benefit from their closer proximity to key emerging markets. In order to maintain competitiveness, investments in productivity enhancing technology, like digital sensors and real-time monitoring systems, as well as automation processes should help improve efficiency, sustainability, reducing waste, and cutting operational costs.

Employment is projected to fall by 0.4% annually. The expected decline in output will translate into a negative outlook for employment. In addition, automation will continue to put downward pressure on the size of the industry’s workforce. Indeed, jobs consisting of repetitive and routine tasks, such as those performed by labourers and operators, should continue to be replaced by machinery.

Challenges and Opportunities

The paper manufacturing industry in Canada is facing significant challenges due to the ongoing digital transformation, which has reduced the demand for traditional paper products, and intense global competition from low-cost producers, especially in emerging markets is South America and Asia. Additionally, stricter environmental regulations and fluctuations in the supply of raw materials are impacting profitability, while economic instability and market fluctuations also amplify risks. Although it was not incorporated into the projections, The United States’ threat to impose new tariffs on imports from Canada constitutes a major source of uncertainty for the pulp and paper sector, which exports a large portion of its production to the United States, and if it materializes, will impose a severe burden on the industry.

However, everything is not all negative for the industry as opportunities emerge in the form of increasing demand for packaging materials driven by e-commerce and the growing market for sustainable products. The industry could benefit from diversifying its products, focusing on higher-value items such as specialty papers and hygiene products, and using technological innovations to improve efficiency and product quality. Despite competition from reusable substitutes, paper-based products maintain an environmentally friendly image, giving them a competitive edge over plastic alternatives.

Real GDP, Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Paper Manufacturing | -0.2 | -0.4 | 0.2 |