Canadian Occupational Projection System (COPS)

Industrial Summary

Printing and Related Activities

(NAICS 3231)

This industry comprises establishments primarily engaged in printing and providing related support activities such as pre-press and bindery work. Printing is among the few manufacturing activities in Canada that are not significantly exposed to changes in global economic conditions and in the value of the Canadian dollar as only 12% of production is shipped to foreign countries, mostly to the United States (80% of exports). The industry employed about 51,000 workers in 2023 (2.8% of total manufacturing employment), largely concentrated in Ontario (47%) and Quebec (28%), with a workforce predominantly composed of men (60%).

Key occupations (5-digit NOC) include:

- Printing press operators (73401)

- Supervisors, printing and related occupations (72022)

- Plateless printing equipment operators (94150)

- Graphic designers and illustrators (52120)

- Binding and finishing machine operators (94152)

- Other labourers in processing, manufacturing and utilities (95109)

- Camera, platemaking and other prepress occupations (94151)

- Graphic arts technicians (52111)

Projections over the 2024-2033 period

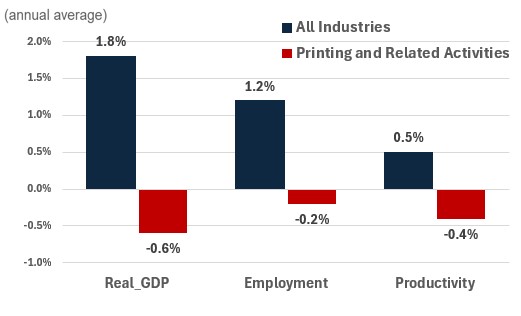

Real GDP is projected to decline at an average annual rate of 0.6%. The industry is expected to continue to face ongoing challenges as digital media continues to gain ground in the communication landscape. Consumers increasingly rely on digital platforms for information and communication, which is replacing printed publication, leading businesses to reduce advertising spending in printed media, further impacting the industry's profitability. On the more positive side, the surging demand for digital content could represent the opportunity for firms to change and diversify their business models to provide more value-added services, including graphic design, logistics, marketing, communication and online content management services.

Productivity is expected to decline at an average annual rate of 0.4%. Historically, productivity has been volatile, but the sector seems to have reached maturity, and potential gains could be expected over the projection period. However, the rise in popularity of digital media and electronic mediums for news is expected to limit investments in the printing and related support activities sector.

Employment is projected to fall by 0.2% annually. With a negative outlook for real GDP, employment is expected to decline as well, but at a slower pace. With the expected reduction in productivity, labour is expected to account for a growing share of production.

Challenges and Opportunities

While the continued adoption of digital media is expected to remain a major challenge for the industry, there are some potential opportunities. The growth in online ordering has resulted in an increased demand for consumer packaging, which in turn requires printed products. Furthermore, while overall print advertising figures have declined, print advertising remains an essential element of many marketing campaigns. Moreover, digital printing has recently emerged as the industry's fastest-growing segment.

The industry will need to look beyond traditional printing methods to capitalize on shifting demand and drive growth. New printing technologies include erasable printing, three-dimensional digital printing for packaging, and jetted-material printing. While these new opportunities are not expected to enable the printing industry to expand over the long term, they could help offset weaker demand for traditional printing. The United States’ threat to impose new tariffs on imports from Canada (which was not incorporated into the projections) may not represent as significant a problem for the industry, as only a relatively small portion of the production is exported. However, it still has the potential to disrupt the sector, as any source of uncertainty might.

Real GDP, Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Printing and Related Activities | -0.6 | -0.2 | -0.4 |