Canadian Occupational Projection System (COPS)

Industrial Summary

Computer, Electronic and Electrical Products

(NAICS 3341-3346; 3351-3359)

This industry comprises establishments primarily engaged in manufacturing information and communications technology (ICT) devices, such as computers and peripherals, telecommunication and audio-video equipment, navigational and measuring instruments, as well as electronic components for such products. It also comprises establishments involved in manufacturing products that generate, distribute and use electrical power, such as generators, transformers, switchgears, batteries, wires, electrical motors and household appliances. ICT is the most important of the two segments, accounting for over half of production in 2023. Overall, the industry is highly export intensive, with about 94% of its revenues coming from abroad, largely from the United States which accounts for 70% of exports. The industry is also largely exposed to import penetration with a substantial share of domestic demand met by imports, mainly from the United States, China and Mexico. It employed about 116,200 workers in 2023 (6.4% of total manufacturing employment), with 63% in the ICT segment. Employment is mostly concentrated in Ontario (49%) and Quebec (28%), and the workforce is predominantly composed of men (71%).

Key occupations (5-digit NOC) include:

- Electronics assemblers, fabricators, inspectors and testers (94201)

- Assemblers and inspectors, electrical appliance, apparatus and equipment manufacturing (94202)

- Electrical and electronics engineers (21310)

- Software engineers and designers (21231)

- Supervisors, electronics and electrical products manufacturing (92021)

- Electrical and electronics engineering technologists and technicians (22310)

- User support technicians (22221)

- Software developers and programmers (21232)

Projections over the 2024-2033 period

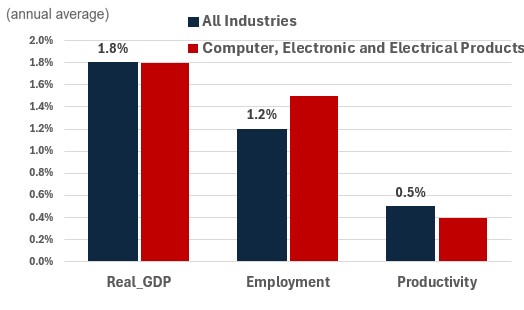

Real GDP is projected to increase at an average annual rate of 1.8%. The demand for computer, electronics and electrical products is expected to continue to be robust, with output projected to grow at a similar rate to the national average. A key driver for the improved industrial outlook is the global renewable energy transition aimed at reducing greenhouse gas emissions, as the sector produces critical inputs such as EV batteries, as well as the increased popularity of smart home devices, such as refrigerators with internet capabilities. High replacement rates and perpetual innovation for many ICT products are also expected to keep driving consumer interest in new products, supporting strong demand.

Productivity is expected to grow at an average annual rate of 0.4%. Increased automation and a shift towards higher value-added products is expected to result productivity growth close to the national average, after the industry has lagged in this regard over the past decade.

Employment is projected to increase by 1.4% annually. As the industry is expected to experience reasonably strong output growth, employment growth is projected to be above both the overall average (1.2%) and the manufacturing average (0.6%). Although certain jobs associated with repetitive and routine tasks may be threatened by increased automation, there could be stronger demand for skilled workers who can operate more complex machinery used in the manufacturing process.

Challenges and Opportunities

In the realm of computer, electronics, and electrical products, staying ahead of new technology trends is essential. Companies that can quickly adapt to and integrate new technologies into their product lines will be better positioned to capture global market share. Given the intense international competition, it is crucial to develop and maintain intellectual property. This requires significant investment in research and development to continuously innovate to maintain a competitive edge in the global market.

Investments in certain subsectors, such as the construction of new factories to produce batteries for EVs, may prove volatile as firms seek to ensure their major infrastructure investments will allow their production supply chains to remain uninterrupted given the changing geopolitical state of manufacturing and free trade in North America.

Real GDP, Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Computer, Electronic and Electrical Products | 1.8 | 1.4 | 0.4 |