Canadian Occupational Projection System (COPS)

Industrial Summary

Architectural, Engineering, Design and Scientific R&D Services

(NAICS 5413; 5414; 5417)

This industry comprises establishments that provide highly specialized business services in three different segments. Architectural, engineering and related services are by far the largest segment, accounting for 74% of production and 71% of employment in 2023. In comparison, specialized design services (which include interior, industrial and graphic design) accounted for only 4% of production, but 15% of employment, versus 22% and 14% respectively for scientific research and development services. The industry employed about 466,200 workers in 2023, mostly concentrated in Ontario (38%), Quebec (21%), Alberta (17%) and British Columbia (16%). The workforce is mainly composed of men (62%), characterized by a high level of educational attainment and a significant proportion of self-employed workers (21%).

The key occupations (5-digit NOC) include:

- Civil engineers (21300)

- Graphic designers and illustrators (52120)

- Other professional engineers, n.e.c. (21399)

- Interior designers and interior decorators (52121)

- Drafting technologists and technicians (22212)

- Architects (21200)

- Mechanical engineers (21301)

- Electrical and electronics engineers (21310)

- Civil engineering technologists and technicians (22300)

- Engineering managers (20010)

- Construction inspectors (22233)

- Geoscientists and oceanographers (21102)

- Land survey technologists and technicians (22213)

- Architecture and science managers (20011)

- Chemical technologists and technicians (22100)

- Petroleum engineers (21332)

- Biologists and related scientists (21110)

- Theatre, exhibit and other creative designers (53123)

- Mechanical engineering technologists and technicians (22301)

- Architectural technologists and technicians (22210)

- Electrical and electronics engineering technologists and technicians (22310)

- Industrial engineering and manufacturing technologists and technicians (22302)

- Chemists (21101)

- Non-destructive testers and inspection technicians (22230)

- Land surveyors (21203)

- Biological technologists and technicians (22110)

- Geological and mineral technologists and technicians (22101)

- Industrial designers (22211)

- Chemical engineers (21320)

- Geological engineers (21331)

- Industrial and manufacturing engineers (21321)

- Physicists and astronomers (21100)

- Landscape architects (21201)

Projections over the 2024-2033 period

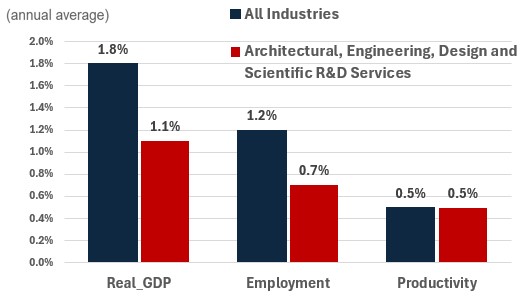

Real GDP is projected to grow at an average annual rate of 1.1%. Elevated interest rates are expected to take a toll on the residential sector and on corporate profits in the short term, limiting demand for architectural, engineering, design and R&D services. However, as interest rates begin declining over the medium-term, growth is expected to resume, bolstered by rising corporate profits, population, and disposable income. Furthermore, with the Investing in Canada Plan still in place until 2028, and the significant emphasis on infrastructure and housing in Budget 2024, federal government spending should continue to drive demand for architectural, engineering and design services[1][2]. To drive growth in R&D, the Government of Canada committed over $4.6 billion to strengthen research and innovation in Canada in Budget 2024, which should drive growth in R&D services[3]. In addition, the continuation of the Scientific Research and Experimental Development (SR&ED) tax incentives should help drive the demand for R&D services.

At the start of 2030, when the oil and gas sector GHG emissions cap becomes mandatory, architectural, engineering, design and R&D services output is projected to fall given that oil and gas is one of the largest purchasers of these services[4]. However, the slowdown is expected to be short-lived. Demand for environmentally conscious designs is likely to keep rising over the next decade, which should help the sector continue to see growth despite the anticipated drop in oil and gas investments. In addition, as Canada continues to work towards net-zero emissions by 2050, the demand for engineering services in the renewable energy space is expected to continue rising, further helping drive growth in output.

Productivity is expected to grow at an average annual rate of 0.5%. In order to remain competitive, both within Canada and internationally, firms in the industry are expected to adopt productivity-enhancing technologies such as building information modeling (BIM) systems to automate much of the work of design and engineering, 3D printing to produce components for modular construction, and drones to monitor and inspect large or difficult-to-access structures. The stronger penetration of AI is also expected to impact productivity growth, complementing and enhancing some of the skills of some professionals typically employed in the sector.

Employment is projected to increase by 0.7% annually. With moderate expectations for output growth, employment growth is also projected to be limited. Although the sector will continue to require a highly educated and specialized workforce, significant employment growth is not anticipated as the sector is expected to adopt productivity improving technologies where possible.

Challenges and Opportunities

COPS expects interest rates to fall in 2024. However, unforeseen events which would cause inflation to rise once again could potentially cause the Bank of Canada to stall cutting rates. Given sector performance is typically reliant on low borrowing costs, this poses a risk to real GDP and employment growth. An opportunity for industry performance is a potential acceleration in our implementation of clean energy infrastructure. In order to meet our emission targets, both the interim 2030 target and net-zero by 2050, Canada needs to invest billions more in renewable energy than assumed in in these COPS projections. Accelerating the creation of this infrastructure would boost demand across the industry with R&D, architects and engineers playing a vital role in the economic transition.

Real GDP , Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Architectural, Engineering, Design and Scientific R&D Services | 1.1 | 0.7 | 0.5 |

[1]Housing, Infrastructure and Communities Canada, Investing in Canada Plan – Building a Better Canada, Government of Canada, June 14, 2024.

[2]Deputy Prime Minister of Canada Chrystia Freeland, Budget 2024: Building homes, communities, and getting major projects done, Government of Canada, June 4, 2024.

[3]Prime Minister of Canada Justin Trudeau, Strengthening Canadian research and innovation, Government of Canada, April 19, 2024.

[4]Environment and natural resources, Regulatory Framework for an Oil and Gas Sector Greenhouse Gas Emissions Cap, Government of Canada, December 7, 2023.