Canadian Occupational Projection System (COPS)

Industrial Summary

Management, Administrative and Other Support Services

(NAICS 5511; 5611-5619; 5621-5629)

This industry is composed of three segments: management of companies and enterprises (including security holdings and head offices); administrative and support services (such as record keeping, employment placement, document preparation, call centres, collection agencies, travel arrangement, and security, janitorial and landscaping activities); and waste management and remediation services (such as the collection, treatment and disposal of waste material, soil remediation, waste water treatment, hazardous material removal). Administrative and support services are the largest and the most labour intensive of the three segments, accounting for 84% of production and 91% of employment in 2023. In comparison, management of companies and enterprises accounted for 2% of production and less than 1% of employment, versus 14% and 8% respectively for waste management and remediation services. The industry employed about 691,600 workers in 2023 (down from 768,100 in 2019), mostly concentrated in Ontario (41%), Quebec (25%), British Columbia (13%) and Alberta (11%). The workforce is characterized by a slight majority of men (56%), and a significant proportion of self-employed (23%) and part-time workers (22%). The industry is also characterized by lower wages than the overall economy average.

Given the wide variety of activities, key occupations (5-digit NOC) include a mix of:

- Light duty cleaners (65310)

- Security guards and related security service occupations (64410)

- Landscaping and grounds maintenance labourers (85121)

- Janitors, caretakers and building superintendents (65312)

- Other customer and information services representatives (64409)

- Contractors and supervisors, landscaping, grounds maintenance and horticulture services (82031)

- Cleaning supervisors (62024)

- Material handlers (75101)

- Travel counsellors (64310)

- Public works maintenance equipment operators and related workers (74205)

- Specialized cleaners (65311)

- Landscape and horticulture technicians and specialists (22114)

- Human resources and recruitment officers (12101)

- Public works and maintenance labourers (75212)

- Court reporters and medical transcriptionists and related occupations (12110)

- Conference and event planners (12103)

- Pest controllers and fumigators (73201)

- Tour and travel guides (64310)

Projections over the 2024-2033 period

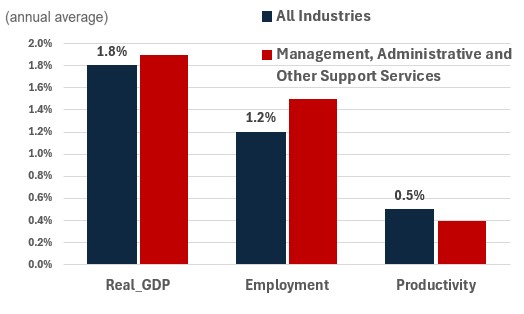

Real GDP is projected to grow at an average annual rate of 1.9%. In the short-term, higher interest rates are expected to keep corporate profits low and to continue to put pressure on per capita disposable income, limiting growth in services to buildings and dwellings, as well as in travel arrangements and reservation services. However, as interest rates begin declining, the Canadian economy should see stronger growth, driving demand for management, administrative and other support services overall. Growth is expected to slow slightly in 2030, however, in response to the mandatory oil and gas GHG emission cap. Given that the oil and gas sector is an important purchaser of management, administrative and other support services, a slowdown in extraction activity in response to the cap will reduce dem[1]and for the sector overall. However, the slowdown is expected to be short-lived. A growing focus on combating climate change and meeting Canada’s target of reaching net-zero emissions by 2050 should help stimulate growth in the sector over the long-term.

Productivity is expected to grow at an average annual rate of 0.4%. %. Janitorial services are expected to increasingly use cleaning robots for certain tasks, and larger cleaning companies are continuing to use software to streamline the scheduling process. However the majority of building maintenance tasks are expected to remain labour intensive. Employment agencies will likely continue to incorporate AI and other technologies to sift through CVs, applications, and job postings to better match employees to the right position. The use of sensor-based waste monitoring, and AI-driven waste management systems will continue to drive productivity gains in the waste management and remediation services subindustry, but similarly is not projected to advance enough to significantly reduce the labour intensity of the sector.

Employment is projected to increase by 1.5% annually. Employment is expected to grow moderately to meet the increase in demand over the coming decade, as technological adoption is expected to result in only moderate productivity over the projection period, as technology has yet to reach the point where it has the potential to fully displace workers in what is currently a highly labour intensive sector.

Challenges and Opportunities

Relatively low wages combined with difficult working conditions in some subsectors have consistently kept the job vacancy rate in the administrative and support, waste management and remediation services portion of the industry (NAICS 56) above the national average. If wages fail to increase sufficiently, employment could rise at a slower pace than currently projected. Although technological improvements could lead to productivity gains, some subindustries, such as employment services, could be negatively impacted by technological change. The rise in popularity of free online recruitment platforms has already impacted employment in the subindustry. Yet, if employment and recruiting agencies cannot prove their efficiency in matching candidates to employers, the demand for services in this subsector could fall as companies continue to favour posting jobs on online job boards.

Real GDP , Employment and Productivity Growth rate (2024-2033)

Sources: ESDC 2024 COPS projections.

| Real GDP | Employment | Productivity | |

|---|---|---|---|

| All Industries | 1.8 | 1.2 | 0.5 |

| Management, Administrative and Other Support Services | 2.2 | 2.4 | -0.2 |

[1]Environment and natural resources, Regulatory Framework for an Oil and Gas Sector Greenhouse Gas Emissions Cap, Government of Canada, December 7, 2023.